Digitization, e-Invoicing, and Currency Circulation – Mode of e-invoicing and Usage of Invoice Software

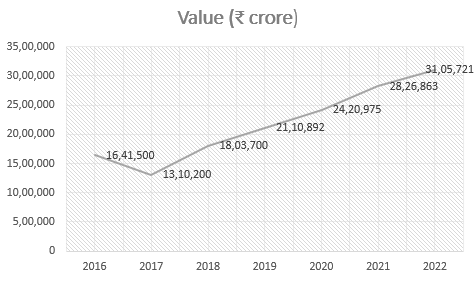

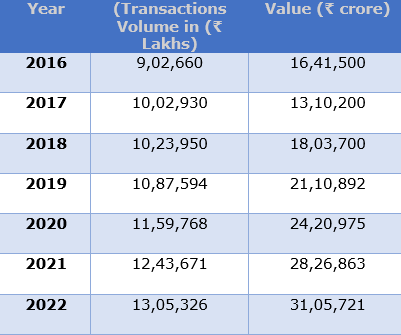

Generally, there is a belief that COVID -19 had significant impact of in currency circulation. The Covid put greater thrust on digitization and dependence on contactless transactions. Also, there was tremendous growth in the usage of UPI, IMPS mode in financial transaction. Many platforms like PhonePe, Google Pay became more popular as alternate modes of fund transfer. Even, there is a belief that the demonization helped in reducing the dependence on hard currency. The demonetization intended to reduce the usage of hard currency in financial transactions. However, the currency circulation is going in an accelerated mode during all the previous years. Currency circulation during the period 2016 – 22 as below.

Currency in Circulation (CiC) includes banknotes and coins. Presently, the Reserve Bank issues notes in denominations of `2, `5, `10, `20, `50, `100, `200, `500 and `2,000. Coins in circulation comprise 50 paise and `1, `2, `5, `10 and `20 denominations. According to RBI report, the volume for the Banknotes in circulation in terms of value, reached INR 31,05,721crores by 2022, almost double prior to demonization.

Currency in circulation is the amount of money that has been issued by monetary authorities minus currency that has been removed from an economy. Currency in circulation is an important component of a country’s money supply. Currency in circulation can consider as currency in hand because it is the money used throughout a country’s economy to buy goods and services. The currency in circulation in a country is determined by the nation’s need or demand for cash. RBI is responsible for ensuring that there is enough money in circulation to meet the economy’s commercial demands, and for releasing additional notes and coins when there is a demand for the same.

Now, with the reduction of threshold limit on e-invoicing to INR 5 crores by Jan 1, 2023, one can expect further control on currency circulation. The process of validating all E-invoices in B2B transactions by the GST Network (GSTN) will push up further digitization in commercial transactions soon the threshold limit is brought down. This will compel all commercial firms to depend on reliable invoice software to run their business since the GSTIN portal needs data points to validate e-invoices. E-invoicing ensures that the invoices generated by accounting software are valid throughout. The system automatically compiles such data during the GST filing process.

The invoice software helps to go for e-invoicing in order to facilitate e-invoicing. Such software generates invoices, transmit the data to GSTin portal. It further pushes up digitization in work environment and reduce the usage of currencies.

SMART ADMIN is a cloud-based software for Office Automation. Smart Admin Tools are designed for Payroll management, Timesheet and Project Tracking – visit SMART ADMIN for FREE Trial and Registration.

For more information visit https://www.smartadmin.co.in/

Attachments

Related Post

Timesheet and Implementation – Change Management...

The digitization of workforce management has emerged as a strategic necessity for Indian organizations, on account of the need for regulator...

Credit and Debit Note under GST...

Everyday business involves numerous transactions in relation to selling goods and providing services. It is mandatory for a GST-registered...

Export of Services and Invoice Format...

The Goods and Services Tax (GST) literature provides detailed guidelines about the content of an invoice in its various notes. The ‘Expo...